Blog

-

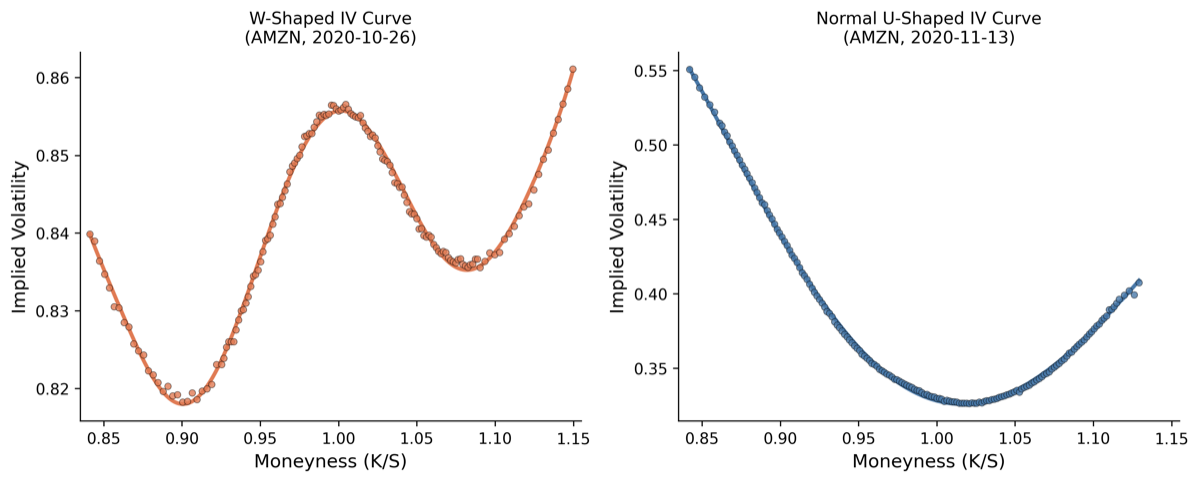

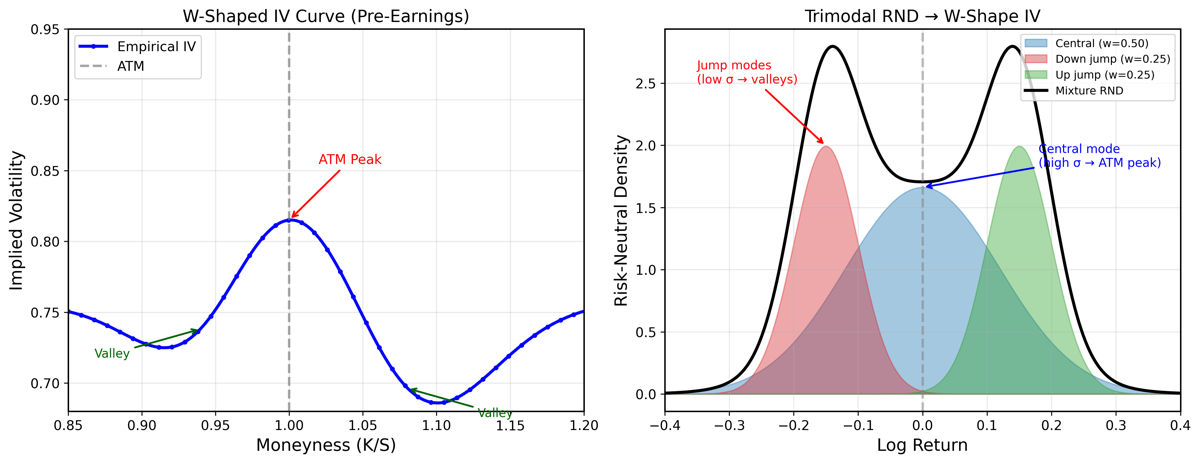

What W-shaped implied volatility tells us about earnings risk

When the IV smile breaks the U and develops a hump near at-the-money, it's a fingerprint of investor uncertainty about the size of an upcoming jump.

Read post → -

When one firm reports, the whole industry's options move

Option markets price an industry-wide uncertainty signal at every earnings announcement — and that signal carries information about the next firm scheduled to report.

Read post → -

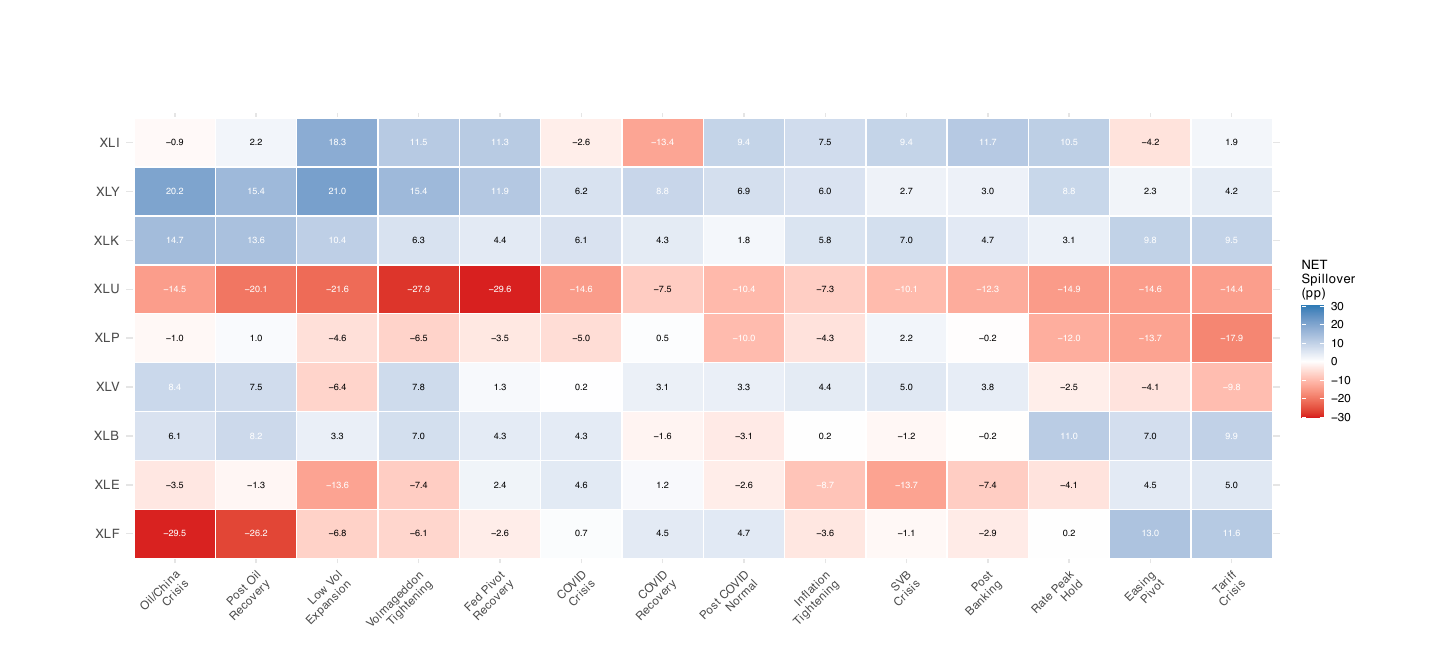

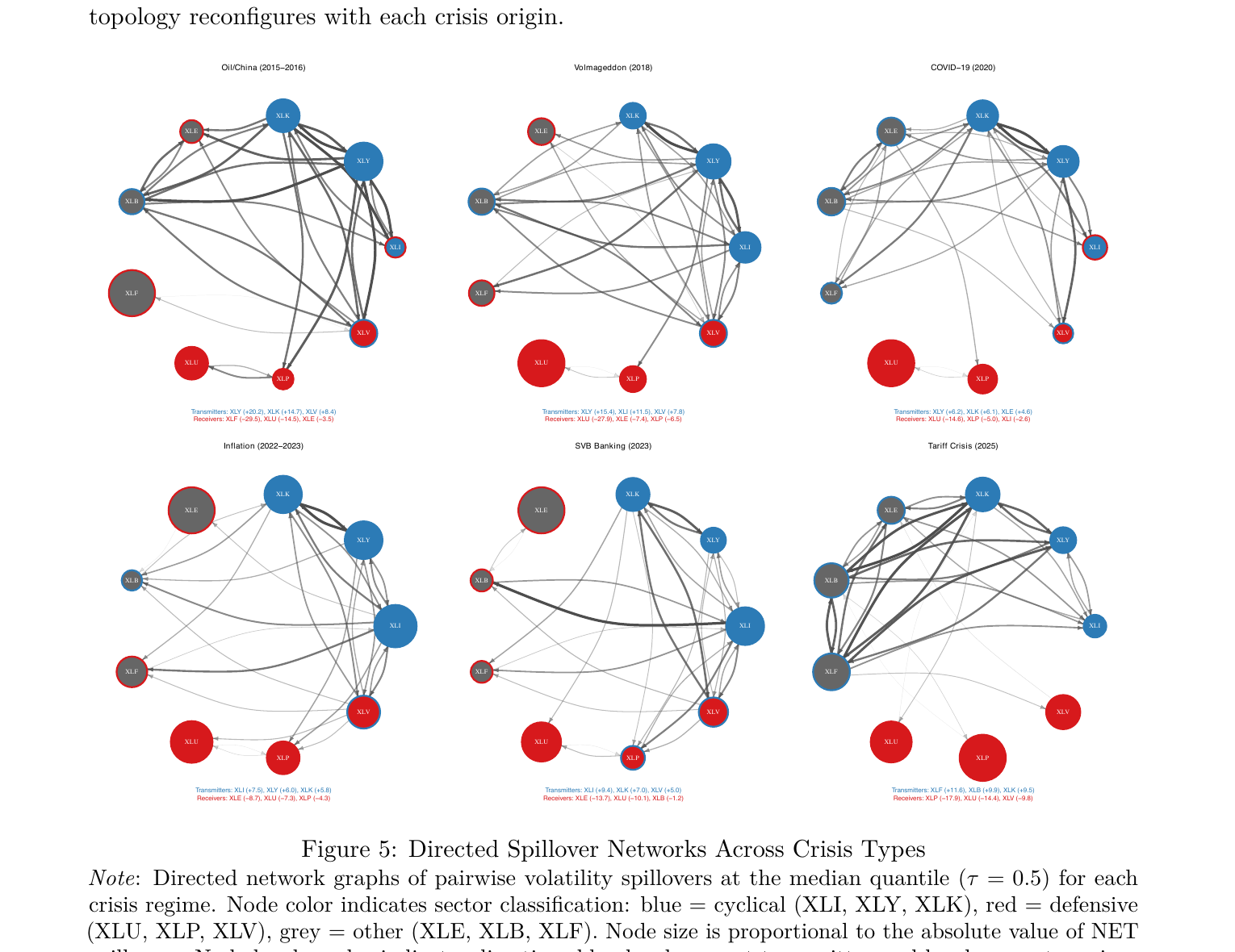

Crisis-origin dependence in sector volatility spillovers

Six U.S. equity-market crises with fundamentally different origins produce six different spillover architectures — but the cyclical-defensive divide holds across every regime.

Read post → -

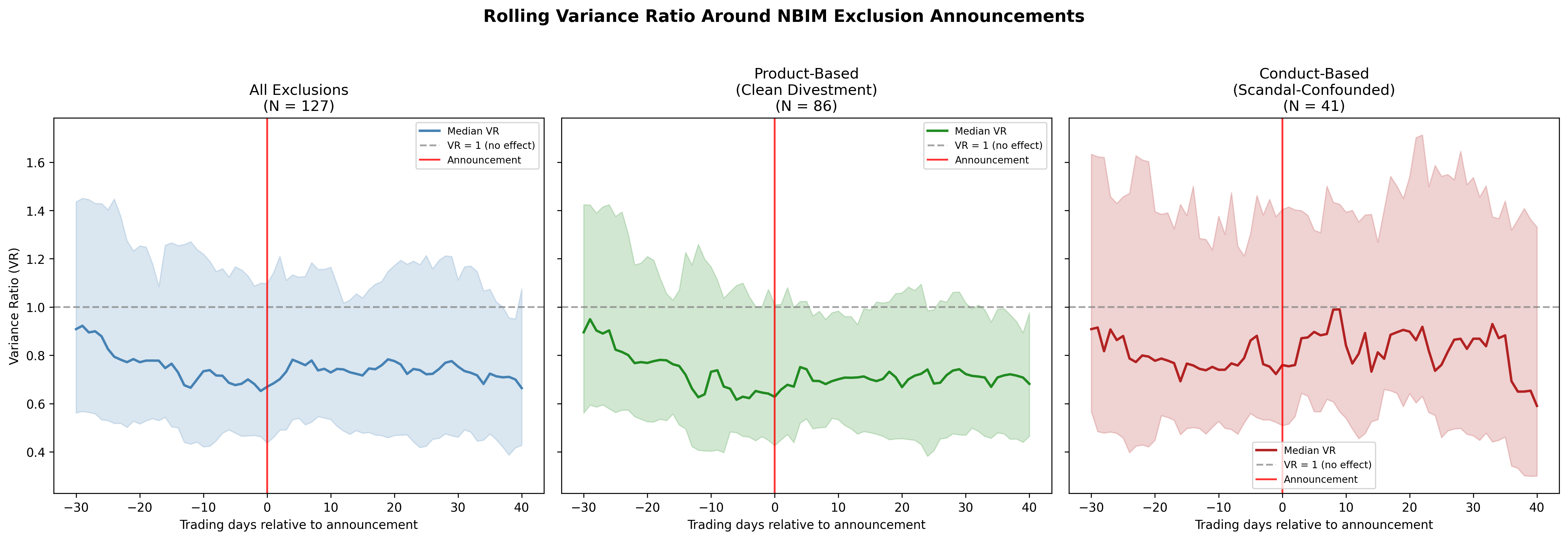

Does divestment move risk? A null result from Norway's $1.7T fund

Theory says institutional divestment should raise firm-level volatility. 181 exclusions by the world's largest sovereign wealth fund say otherwise — and the bounds on the true effect are very tight.

Read post →