Does divestment move risk? A null result from Norway's $1.7T fund

The case for ESG divestment usually rests on two theoretical channels. The first is well-known: pulling capital out of a firm raises its cost of capital and depresses its share price. The second is less discussed but mechanically just as old: removing a large investor narrows the marginal-investor pool, which standard equilibrium-pricing arguments say should raise the firm’s idiosyncratic volatility.

The first channel — cost of capital — was tested decisively against the largest natural experiment available, and Berk and van Binsbergen (2025) found nothing. This paper runs the same kind of test for the second channel — volatility — using the same natural experiment, and finds the same thing: nothing.

That is the headline. The interesting parts are which tests detect nothing, how tightly the null is bounded, and what’s left of the underlying theory once both channels come up empty.

The natural experiment

Norway’s Government Pension Fund Global (GPFG) manages roughly $1.7T in assets and follows a well-publicized exclusion process. The Council on Ethics investigates a candidate firm, recommends exclusion to the Norges Bank Executive Board, and the Board makes a final decision that is publicly announced. Over the sample period this paper exploits, GPFG had excluded 181 individual firms.

Two features make this useful:

- The fund is genuinely large. GPFG holds, on average, around 1.5% of global listed equity. When it exits a position, that is a non-trivial supply shock for the underlying firm.

- Exclusions split cleanly into two types. Product-based exclusions (tobacco, certain weapons categories, thermal coal) trigger automatically on a firm’s business activity, with no underlying scandal or governance event attached. Conduct-based exclusions are tied to specific ESG controversies — environmental damage, corruption, human-rights violations — that a researcher trying to isolate the divestment channel would have to disentangle from the news event itself.

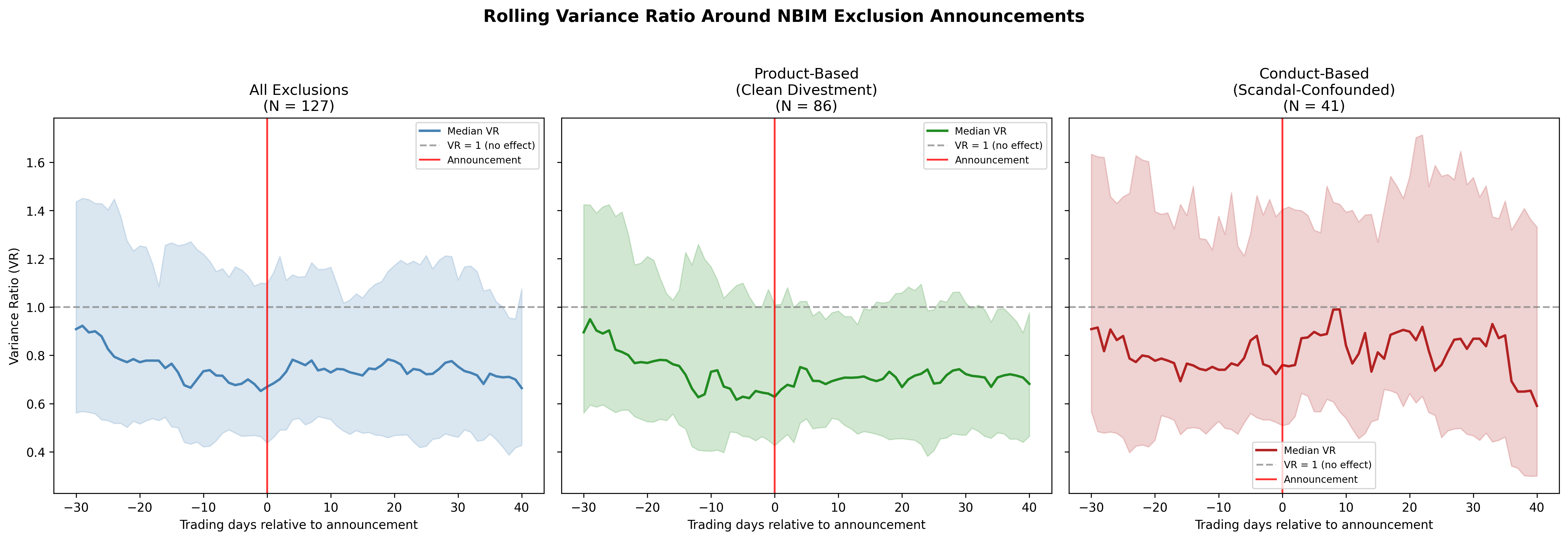

The product-based subset is what makes this test possible. There is no confounding event; the only thing happening at announcement is the divestment itself. If volatility responds to divestment as a clean mechanism, you should see it here.

What the GARCH test does

The cleanest first-pass test compares conditional volatility before and after the announcement. Fit a standard GARCH(1,1) to each firm’s return series and compute the variance ratio across the announcement window:

Under the null of no divestment effect, is centered at one. Under the theoretical prediction, should be reliably above one — particularly for the product-based subset, where there is no countervailing news.

It isn’t. Across the full sample, across the product-based sub-sample, across the investigation period (when the Council on Ethics is reviewing the firm but no announcement has been made), the variance ratio is statistically indistinguishable from one. Sign-test versions and rank-test versions give the same answer.

A natural rebuttal: “GARCH(1,1) is too rigid; the real volatility process has a structural break that the GARCH model smooths over.” So the paper runs a panel difference-in-differences specification with an event-window indicator and firm × month fixed effects, on raw realized volatility. The DiD coefficient is small and insignificant. Switching realized volatility for range-based volatility, or tightening the event window, does not change the conclusion.

Why “fail to reject” is not enough

A standard difference-in-differences null result is hard to interpret. You did not reject — but is that because the effect is genuinely zero, or because your test is underpowered against an effect that is real but small?

The right tool here is an equivalence test, which inverts the standard hypothesis structure: rather than testing whether the effect equals zero, you specify a smallest effect size you would care about and test whether the true effect is bounded inside that interval.

Two-one-sided-tests (TOST) at conventional levels deliver tight bounds. With an equivalence margin set at one-tenth of the in-sample volatility standard deviation — a magnitude that would still be uneconomic from a practitioner’s standpoint — the data tightly reject any effect outside that band. The true effect is not just statistically zero; it is meaningfully zero.

That is the difference between “we couldn’t find it” and “it isn’t there.”

Combined with the cost-of-capital null

If divestment did neither of the two things the theory predicts — neither raise the cost of capital (Berk and van Binsbergen 2025) nor raise idiosyncratic volatility (this paper) — then the question becomes: what does divestment do?

A few candidates remain on the table:

- Reputational pressure on management. This is a behavioral channel, not a pricing channel, and the announcement-effects literature does see modest evidence for it.

- Coordination effects on other investors. GPFG’s exclusion lists are widely watched and explicitly used by other institutional asset owners as a screen. The pricing impact of that aggregated exit, rather than GPFG’s individual exit, would show up in the long run rather than in announcement windows. The current data cannot rule this in or out.

- Nothing measurable in financial markets. This is the read I find hardest to argue against. The two cleanest pricing-theory predictions both fail. Whatever divestment is doing, it is not showing up in the prices.

The paper is careful not to over-claim. The null result is about the Norwegian fund’s exclusion mechanism, in the announcement window and the short-to-medium post-announcement window, on publicly traded equity markets. It does not say divestment is ineffective for changing corporate behavior, nor that it is uninformative for end investors who care about non-pecuniary returns.

What it does say is that the textbook financial-economics case for divestment-as-a-pricing-tool is, on the best available evidence, empirically inactive.

What I’d read next

- Berk, Jonathan B., and Jules H. van Binsbergen (2025), “The Impact of Impact Investing.” The companion null. Same natural experiment, cost-of-capital channel, same answer.

- Pástor, Ľuboš, Robert F. Stambaugh, and Lucian A. Taylor (2021), “Sustainable Investing in Equilibrium.” The cleanest theoretical statement of both the cost-of-capital and the volatility channels. Read alongside the two empirical nulls and decide for yourself.

- Hartzmark, Samuel M., and Kelly Shue (2023), “Counterproductive Sustainable Investing.” A different cut at the same problem — argues that capital-allocation pressure on already-clean firms can have counterproductive effects.

- Norges Bank Investment Management exclusion list. Public. Reading through the case-by-case justifications is the best way to develop intuition about what GPFG is actually doing — and why it does not, mechanically, look like the kind of shock the theory imagines.

The full paper is at /papers/divestment-volatility.pdf. Working paper, 2026. Comments welcome — simen.guttormsen@nmbu.no.